All Categories

Featured

Table of Contents

There is no payment if the plan expires prior to your fatality or you live beyond the policy term. You may have the ability to restore a term policy at expiration, yet the costs will be recalculated based upon your age at the time of revival. Term life insurance policy is usually the least costly life insurance policy available because it supplies a fatality benefit for a limited time and doesn't have a money worth element like irreversible insurance.

At age 50, the costs would certainly climb to $67 a month. Term Life Insurance policy Fees 30 years old $18 $15 40 years old $28 $23 50 years old $67 $51 Source: Quotacy. Quotes are for a $250,000 30-year term life plan, for guys and women in outstanding health and wellness.

A Term Life Insurance Policy Matures Upon Endowment Of The Contract

The minimized danger is one aspect that enables insurance firms to bill lower costs. Rate of interest, the financials of the insurance provider, and state laws can also influence costs. As a whole, firms frequently provide much better prices at the "breakpoint" insurance coverage levels of $100,000, $250,000, $500,000, and $1,000,000. When you think about the quantity of protection you can get for your premium bucks, term life insurance tends to be the least expensive life insurance policy.

He buys a 10-year, $500,000 term life insurance plan with a premium of $50 per month. If George dies within the 10-year term, the plan will pay George's recipient $500,000.

If George is diagnosed with a terminal health problem during the initial plan term, he probably will not be qualified to renew the plan when it expires. Some policies provide ensured re-insurability (without proof of insurability), yet such attributes come at a greater cost. There are a number of kinds of term life insurance policy.

Typically, many business use terms ranging from 10 to thirty years, although a few offer 35- and 40-year terms. Level-premium insurance coverage (when a ten year renewable term life insurance policy issued at age 45) has a set regular monthly payment for the life of the policy. A lot of term life insurance policy has a level premium, and it's the type we've been describing in the majority of this post.

Term Life Insurance Uk

Term life insurance is eye-catching to youths with children. Moms and dads can acquire considerable coverage for an inexpensive, and if the insured dies while the plan is in result, the family members can rely upon the survivor benefit to change lost income. These plans are also fit for individuals with expanding family members.

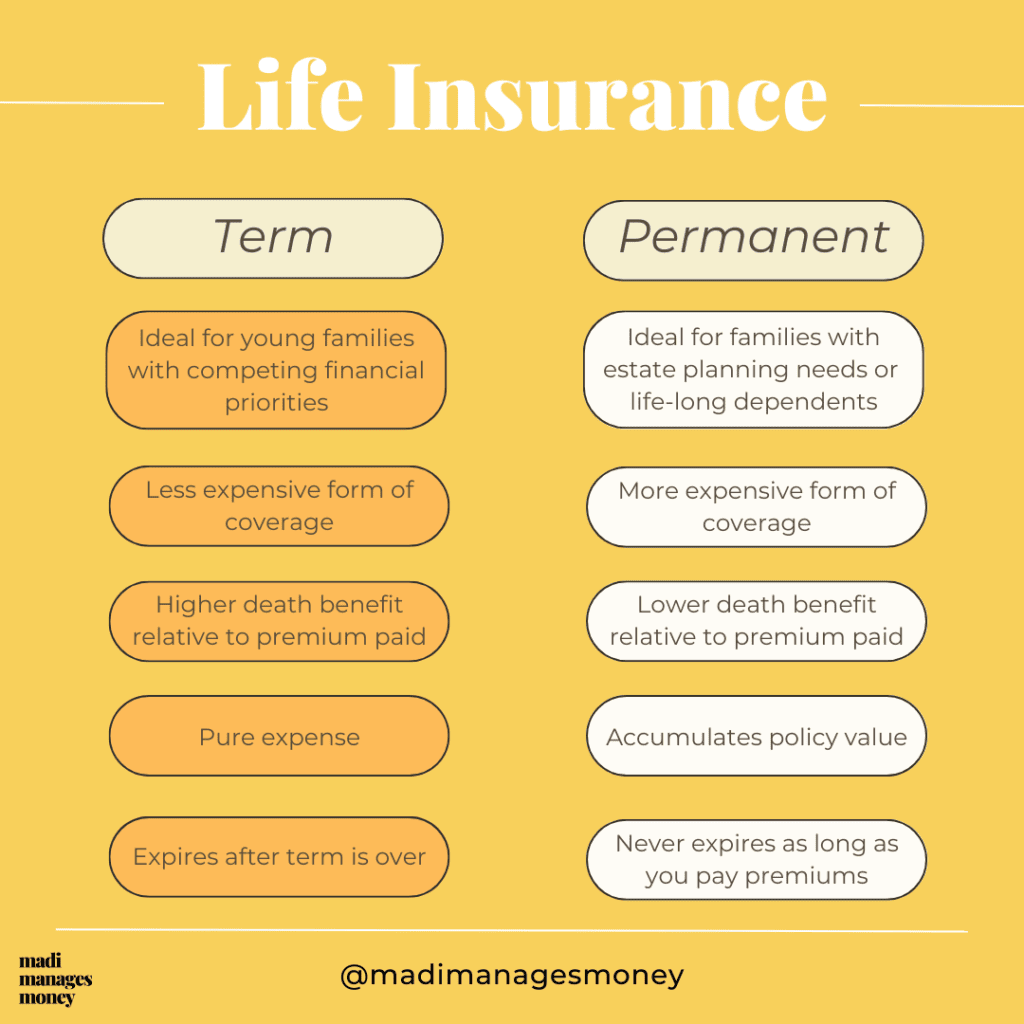

The appropriate choice for you will rely on your demands. Here are some points to consider. Term life policies are perfect for individuals who want substantial coverage at an inexpensive. People that own whole life insurance policy pay extra in premiums for less coverage but have the security of knowing they are safeguarded permanently.

The conversion rider ought to enable you to transform to any kind of long-term policy the insurer provides without limitations - voluntary term life insurance. The key functions of the cyclist are keeping the original wellness rating of the term policy upon conversion (even if you later on have health issues or come to be uninsurable) and determining when and how much of the coverage to transform

Of course, general costs will certainly raise dramatically because whole life insurance coverage is extra costly than term life insurance coverage. Medical conditions that establish throughout the term life duration can not trigger costs to be enhanced.

Entire life insurance policy comes with significantly greater monthly costs. It is suggested to give insurance coverage for as lengthy as you live.

Decreasing Term Life Insurance Example

It depends upon their age. Insurance provider set a maximum age limit for term life insurance coverage policies. This is normally 80 to 90 years of ages however may be higher or lower depending upon the company. The premium also climbs with age, so an individual aged 60 or 70 will certainly pay considerably more than somebody years more youthful.

Term life is rather comparable to car insurance. It's statistically not likely that you'll need it, and the premiums are money down the drainpipe if you don't. If the worst occurs, your family will receive the advantages.

This plan layout is for the client that needs life insurance policy yet would love to have the capacity to choose how their cash money value is invested. Variable plans are financed by National Life and dispersed by Equity Providers, Inc., Registered Broker/Dealer Associate of National Life Insurance Policy Company, One National Life Drive, Montpelier, Vermont 05604.

For J.D. Power 2024 honor details, check out Permanent life insurance policy creates money value that can be obtained. Plan financings accumulate rate of interest and unpaid policy car loans and interest will minimize the survivor benefit and cash value of the policy. The quantity of money worth offered will normally rely on the kind of irreversible policy purchased, the quantity of insurance coverage purchased, the length of time the plan has been in force and any type of impressive policy lendings.

Which Of The Following Are Characteristics Of Term Life Insurance?

A total declaration of protection is discovered only in the policy. Insurance policies and/or linked bikers and attributes might not be available in all states, and plan terms and problems may differ by state.

The main differences in between the various kinds of term life plans on the marketplace have to do with the size of the term and the coverage amount they offer.Level term life insurance comes with both level costs and a degree death benefit, which means they stay the very same throughout the duration of the plan.

It can be restored on an annual basis, however costs will boost every single time you restore the policy.Increasing term life insurance policy, additionally called an incremental term life insurance strategy, is a plan that includes a survivor benefit that boosts with time. It's normally more complex and pricey than degree term.Decreasing term life insurance includes a payout that reduces gradually. Usual life insurance term lengths Term life insurance coverage is economical.

The main differences in between term life and entire life are: The size of your insurance coverage: Term life lasts for a collection period of time and then runs out. Average regular monthly entire life insurance coverage rate is determined for non-smokers in a Preferred wellness category, getting an entire life insurance coverage policy paid up at age 100 supplied by Policygenius from MassMutual. Aflac uses various long-lasting life insurance coverage policies, consisting of entire life insurance coverage, last cost insurance policy, and term life insurance.

{kind=link}

Table of Contents

Latest Posts

Blended Term Life Insurance

Types Of Burial Insurance

Funeral Coverage Insurance

More

Latest Posts

Blended Term Life Insurance

Types Of Burial Insurance

Funeral Coverage Insurance